Marginal Dishonesty: The Adding-to-10 Task

Overview

Source: Julian Wills & Jay Van Bavel—New York University

Classical economic theory asserts that people are rational and self-interested. In addition to seeking wealth and status, people are motivated by other goals. As a result, financial motives can sometimes be dwarfed by other internal needs, such as maintaining a positive self-concept or affiliating with other group members.

Ethical dilemmas, such as the temptation to cheat on taxes, can result when these motives are in conflict. On the one hand, people may be tempted to save money by underreporting their taxable income. On the other hand, no one wants to perceive themselves as a dishonest, free-rider. As a result, people are reluctant to fully exploit unethical opportunities because doing so can severely undermine their self-image as morally upstanding individuals. Instead, people cheat to a much smaller degree than they are capable of: just enough to gain additional resources, but not so much as to compromise their self-image.

This tendency for marginal dishonesty, or the "fudge factor," is an important principle in social psychology and can be tested through a variety of techniques. Mazar, Amir, and Ariely originally described six separate experiments involving (dis)honesty and a theory of self-concept maintenance.1 The "Adding-to-10 Task" is one of the experimental techniques discussed and is prevalent in research that involves testing honesty. This video demonstrates how to produce and interpret the Adding-to-10 Task.

Principles

Principles of honesty are rooted in the philosophies of Thomas Hobbes and Adam Smith. Modern economic models espouse the belief that people behave dishonestly by consciously weighing the benefits versus the costs of the dishonest acts. This cost-benefit analysis considers possible external rewards, the probability of being caught and the magnitude of possible punishment. Psychologists build upon the economic model by introducing the effect of internal rewards. When people comply with their internal values systems, derived from society norms, they are provided with positive rewards, whereas noncompliance results in negative rewards, i.e., punishment. This internal reward system affects people's self-concept, their self-perception which is influenced greatly by notions of morality.

Procedure

1. Participant Recruitment

- Conduct a power analysis and recruit a sufficient number of participants.

- Randomly assign half the participants to the experimental condition and the other half to the control condition.

2. Data Collection

- Give participants a test booklet with twenty matrices from the Adding-to-10 Task.

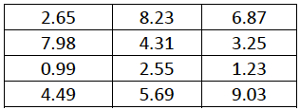

- Each matrix is based on a set of twelve three-digit numbers, two of which sum exactly to 10 (see Figure 1 for example).

- This task is beneficial because the answers are unambiguous.

Figure 1: One of the more common test stimuli used to elicit the fudge factor is the Adding-To-10 Task. Participants are instructed to find two numbers that add to ten in each matrix (e.g., 4.31 and 5.69 in the example above).

- Inform participants that, at the end of the session, two randomly selected participants will receive a bonus payment of $10 for each correctly solved matrix.

- Explain to participants that their goal is to circle the two numbers on each matrix that add to 10 and to complete as many as possible within 4 min.

- It is imperative that the test is challenging enough so that most participants are unable to correctly answer all questions in the allotted time.

- Call time after 4 min and instruct the participants to stop writing.

- For the control condition: Collect test booklets directly from participants. Verify and record the number of questions correctly answered.

- This will ensure that participants in the control condition have no opportunity to cheat.

- In the experimental condition: Read the correct answers to participants and allow them to 'grade' their own performance.

- Instruct them to tear off the back blank page of the booklet and write their name and number of total correct answers.

- Further instruct them to leave their answer page on the front desk and then dispose of, or take with them, the booklet.

- This provides the experimental group with an opportunity to cheat since the answers they actually recorded in the booklets cannot be verified.

- Fully debrief participants.

3. Data Analysis

- For the dependent measure, calculate the performance of both conditions by counting the number of correctly answered questions (control condition) versus the number of correctly answered questions reported(experimental condition).

- The control condition provides a baseline estimate since there is no opportunity to cheat. If people exploit the opportunity to cheat, then the number of correct answers reported in the experimental condition will be larger in comparison.

Results

This procedure typically results in a considerably higher number of correctly "solved" questions in the experimental condition (Figure 2). This procedure can also dissociate whether this inflated performance is a result of a few individuals cheating a lot or most individuals cheating a little bit. If the former were true, this would result in a mostly overlapping distribution except for a large relative increase of individuals reporting the highest possible score. Instead, typical results reveal that most participants cheat a little bit.

Figure 2: A typical frequency distribution resulting from the task. In this example, there is one experimental condition and one control condition with no opportunity to cheat. The y-axis values reflect the proportion of individuals who reported correctly solving a specific number of test questions. Values on the x-axis represent bins of three numbers centered on the label displayed (e.g., 30 = participants who solved 29, 30, or 31 questions).

Application and Summary

People inherently are torn between achieving gains from cheating versus maintaining a positive self-concept of honesty. By using techniques like the Adding-to-10 Task, modern psychological research concludes that often people, who think highly of themselves in terms of honesty, will rationalize their behavior in such a way to allow them to engage in limited dishonesty while maintaining positive views of themselves. Put another way, there is an acceptable level of dishonesty that is defined by internal reward considerations. Given these factors, dishonesty may actually decrease as external rewards increase, i.e., the internal punishment does not kick in until a certain level of gain is achieved.

Economists estimate that dishonest behaviors (e.g., cheating on tax returns, returning clothing after use, employee theft, etc.) cost organizations billions of dollars each and every year. Legislative regulations that penalize dishonesty can be expensive and exploited. In contrast, research suggests that interventions that appeal to our motives for self-image maintenance may be cheaper and more effective. For instance, research suggests that subtly priming people's self-awareness (e.g., placing a mirror behind a jar of money) can reduce theft.2

These findings also cohere with one of the core tenets of social psychology: Almost everyone is capable of misbehaving depending on the situation. Efforts to discourage cheating might be more effective if they focus less on the rare master-mind criminal and instead address the possibility that most people cheat slightly. Interventions that draw attention to ordinary people's self-image may be fruitful for reducing this temptation. For instance, Mazar et al. found that priming participants with The Ten Commandments dramatically reduced cheating (even among atheists).

References

- Mazar, N., Amir, O., & Ariely, D. (2008). The dishonesty of honest people: A theory of self-concept maintenance. Journal of Marketing Research, 45, 633-644.

- Ariely, D. (2012). The (honest) truth about dishonesty: How we lie to everyone-especially ourselves. HarpersCollins. New York.

Tags

Skip to...

Videos from this collection:

Now Playing

Marginal Dishonesty: The Adding-to-10 Task

Social Psychology

6.3K Views

Analyzing Situations in Helping Behavior

Social Psychology

41.9K Views

Using fMRI to Dissect Moral Judgment

Social Psychology

11.4K Views

Perspectives on Social Psychology

Social Psychology

8.5K Views

Evaluating the Accuracy of Snap Judgments

Social Psychology

21.0K Views

A Minority of One: Conformity to Group Norms

Social Psychology

17.3K Views

Misattribution of Arousal and Cognitive Dissonance

Social Psychology

16.7K Views

Ostracism: Effects of Being Ignored Over the Internet

Social Psychology

10.6K Views

Inducing Emotions

Social Psychology

15.6K Views

Persuasion: Motivational Factors Influencing Attitude Change

Social Psychology

25.7K Views

Creating the Minimal Group Paradigm

Social Psychology

25.6K Views

The Implicit Association Test

Social Psychology

52.4K Views

Nonconscious Mimicry Occurs when Affiliation Goals are Present

Social Psychology

7.9K Views

Effects of Thinking Abstractly or Concretely on Self-control

Social Psychology

6.5K Views

Thinking Too Much Impairs Decision-Making

Social Psychology

11.0K Views

Copyright © 2025 MyJoVE Corporation. All rights reserved